Cell-free DNA Testing Market Report 2017–2023

- November, 2017

- Domain: Healthcare - Diagnostics

- Get Free 10% Customization in this Report

Cell-free DNA Testing Market By Test Type (Non-invasive prenatal testing, Circulating tumour DNA, Donor-derived cell-free DNA): By Application (Prenatal Testing, Cancer, Transplantation diagnostics): By region (North America, Europe, Asia Pacific and Rest of the world) – Global Drivers, Restraints, Opportunities, Trends, and Forecasts: 2017–2023

Overview:

Cell-free DNA (cfDNA) are non-encapsulated fragments of DNA molecule present in blood and urine that has huge screening and diagnostic applications. CfDNA is used for fetal DNA screening tests to detect chromosomal abnormalities, as a biomarker for specific mutations detection in cancer patients, as a biomarker to detect post transplantation rejection, and other applications. According to the Center of Disease Control and Prevention, around 6,000 babies are born with Down syndrome every year that is nearly 1 in every 700 babies and the disease incidence is increased by about 30% between 1979 and 2003. Further, according to the study by World Health Organization, approximately 14 million new cancer cases were diagnosed and is expected to grow by about 70% over the next 2 decades.

The cfDNA testing market is booming due to advanced maternal age, increasing number of chronic diseases, change in lifestyle that leads to lifestyle diseases like cancer, and unhealthy food habits. The rising disease incidence along with the increasing medical spending and healthcare expenditure provide opportunities for molecular diagnostics company to come up with more number of innovative tests in the market. However, there is a huge market space for molecular diagnostic companies to come up with novel tests directing on transplantation rejection cases like liver, lung, etc, in the near future.

Market Analysis:

The “Global Cell-free DNA Testing Market” is estimated to witness a CAGR of 26.5% during the forecast period 2017–2023. The market is analyzed based on three segments, namely test types, application, and regions.

Regional Analysis:

The regions covered in the report are North America, Europe, Asia Pacific, and Rest of the World (RoW). The Americas is set to be the leading region for the cfDNA testing market growth followed by Europe. Asia Pacific and RoW are set to be the emerging regions.

Test Types Analysis:

The global cfDNA testing market by test type is segmented into Non-invasive prenatal testing, circulating tumor DNA tests, and donor-derived cell-free DNA tests. Non-invasive prenatal testing is the largest segment, as women are more career-oriented, and the trend is seen in western countries to start family at a late age. These lead to an increase in the average maternal age. Donor-derived cfDNA tests are the fastest growing segment. The rising number of organ donors, increasing transplantation procedures, increasing healthcare awareness have made them the fastest growing segment of the market. The market is also witnessing various acquisitions, agreements, and new product launches and collaborations among the top players, which is defining the future of the global cfDNA testing market.

Application Analysis:

The global cfDNA testing market by application is segmented into Prenatal testing, cancer and Transplantation diagnostics. Prenatal testing occupies the largest market share and transplantation is expected to be the fastest growing segment during the forecasted period.

Key Players:

Natera, Inc., Beijing Genomics Institute, F. Hoffmann-La Roche (Roche), Laboratory Corporation of America Holdings, Illumina, Inc., Guardant Health, Trovagene, Inc., Biocept, Inc., and other predominate & niche players.

Competitive Analysis:

Currently, the cfDNA tests dominate the global cfDNA testing market. A lot of new players are focusing on this market to provide innovative tests with high accuracy and less turnaround time. Many major players in the market are launching new products to maintain their leadership in the market. Apart from this, the big players are acquiring small companies in the market to enhance their product portfolio and maintain their market leadership. For instance, in September 2016, LabCorp acquired Sequenom to strengthen its non-invasive prenatal testing product portfolio.

Benefits:

The report provides complete details about the usage and adoption rate of cfDNA tests in various applications and regions. With that, the key stakeholders can know about the major trends, drivers, investments, vertical player’s initiatives, government initiatives toward the test adoption in the upcoming years along with the details of commercial tests available in the market. Moreover, the report provides details about the major challenges that are going to impact the market growth. Additionally, the report gives complete details about the key business opportunities to key stakeholders to expand their business and capture the revenue in the specific verticals to analyze before investing or expanding the business in this market.

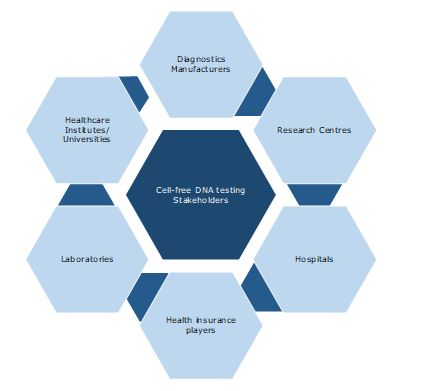

Key Stakeholders:

1 Industry Outlook

1.1 Industry overview

1.2 Total addressable market

1.3 Industry Trends

2 Report Outline

2.1 Report Scope

2.2 Report Summary

2.3 Research Methodology

2.4 Report Assumptions

3 Market Snapshot

3.1 Market Definition – Infoholic Research

3.2 Importance of Cell-Free DNA testing

3.3 Complications of Cell-Free DNA testing

3.4 Segmented Addressable Market (SAM)

3.5 Industry Trends

3.6 Related Markets

3.6.1 Liquid biopsy market

3.6.2 Transplantation Diagnostics Market

4 Market Outlook

4.1 Overview

4.2 Regulatory framework

4.3 Funding scenario

4.4 Market segmentation

4.5 PEST Analysis

4.6 Porter 5(Five) Forces

5 Market Characteristics

5.1 DRO – Global Cell-free DNA testing Market Dynamics

5.1.1 Drivers

5.1.1.1 Rising incidence of babies with chromosomal disorders due to increasing number of late pregnancies

5.1.1.2 Rising number of cancers

5.1.1.3 Growing demand through non-invasive procedures for early disease diagnosis

5.1.2 Opportunities

5.1.2.1 Increase healthcare spending and growing healthcare awareness in emerging countries

5.1.2.2 Increase in mergers & acquisitions

5.1.3 Restraints

5.1.3.1 High test cost with less reimbursement facilities

5.1.3.2 Ethical issues

5.1.3.3 Lack of skilled professionals for performing advanced diagnostic testing

6 Test Types: Market Size and Analysis

6.1 Overview

6.2 Non-invasive prenatal testing (NIPT)

6.3 Circulating tumour DNA tests

6.4 Donor-derived cell free DNA tests

7 Application: Market Size and Analysis

7.1 Overview

7.2 Prenatal testing

7.3 Cancer

7.4 Transplantation diagnostics

8 Regions: Market Size and Analysis

8.1 Overview

8.2 North America

8.2.1 Overview

8.2.2 United states

8.2.3 Canada

8.3 Europe

8.3.1 Overview

8.3.2 United Kingdom

8.3.3 Germany

8.3.4 France

8.3.5 Spain

8.4 APAC

8.4.1 Overview

8.4.2 India

8.4.3 China

8.5 Rest of the World

8.5.1 Overview

8.5.2 Brazil

8.5.3 Middle East

9 Competitive Landscape

9.1 Overview

10 Vendor Profiles

10.1 Natera, Inc.

10.1.1 Overview

10.1.2 Natera Inc.:Product offerings

10.1.3 NATERA, INC.: Recent Developments

10.1.4 Geographic Presence

10.1.5 Business Focus

10.1.6 SWOT Analysis

10.1.7 Business Strategy

10.2 Laboratory Corporation of America Holdings (LABCORP)

10.2.1 Overview

10.2.2 Laboratory Corporaton Of America Holdings: Product Offerings

10.2.3 Laboratory Corporation Of America Holdings: Recent Developments

10.2.4 Business Unit

10.2.5 Geographic Presence

10.2.6 Business Focus

10.2.7 SWOT Analysis

10.2.8 Business Strategy

10.3 Illumina, Inc.,

10.3.1 Overview

10.3.2 Illumina, INC: Product offerings

10.3.3 Illumina, INC: Recent Developments

10.3.4 Geographic Presence

10.3.5 Business Focus

10.3.6 SWOT Analysis

10.3.7 Business Strategy

10.4 BEIJING GENOMICS INSTITUTE

10.4.1 Overview

10.4.2 Beijing Genomics Institute: Product offerings

10.4.3 Beijing Genomics Institute: Recent Developments

10.4.4 Business Focus

10.4.5 SWOT Analysis

10.4.6 Business Strategy

10.5 F.Hoffmann-La Roche Ltd

10.5.1 Overview

10.5.2 F. Hoffmann-la Roche: Product Offerings

10.5.3 F. Hoffmann-la roche.: Recent Developments

10.5.4 Business Unit

10.5.5 Geographic Presence

10.5.6 Business Focus

10.5.7 SWOT Analysis

10.5.8 Business Strategy

Companies to Watch For

10.6 CareDx, Inc

10.6.1 Overview

10.6.2 caredx: Recent Developments

10.7 LifeCodexx AG

10.7.1 Overview

10.7.2 LifeCodexx AG: Recent Developments

10.8 Biocept, Inc.

10.8.1 Overview

10.8.2 Biocept, Inc.: Recent Developments

10.9 Quest Diagnostics

10.9.1 Overview

10.9.2 Quest Diagnostics: Recent Developments

10.10 Guardant Health

10.10.1 Overview

10.10.2 Guardant Health: Recent Developments

10.11 Inivata Limited

10.11.1 Overview

10.11.2 Inivata Limited: Recent Developments

10.12 Personal Genome Diagnostics

10.12.1 Overview

10.12.2 Personal Genome Diagnostics: Recent Developments

10.13 Trovagene

10.13.1 Overview

10.13.2 Trovagene, Inc.: Recent Developments

Annexure

Abbreviations

Research Framework

Infoholic research works on a holistic 360° approach in order to deliver high quality, validated and reliable information in our market reports. The Market estimation and forecasting involves following steps:

- Data Collation (Primary & Secondary)

- In-house Estimation (Based on proprietary data bases and Models)

- Market Triangulation

- Forecasting

Market related information is congregated from both primary and secondary sources.

Primary sources

involved participants from all global stakeholders such as Solution providers, service providers, Industry associations, thought leaders etc. across levels such as CXOs, VPs and managers. Plus, our in-house industry experts having decades of industry experience contribute their consulting and advisory services.

Secondary sources

include public sources such as regulatory frameworks, government IT spending, government demographic indicators, industry association statistics, and company publications along with paid sources such as Factiva, OneSource, Bloomberg among others.

![]()