Global Cancer Diagnostics Market 2018-2024

- December, 2017

- Domain: Healthcare - Diagnostics

- Get Free 10% Customization in this Report

Overview: Cancer diagnostic testing involves tests and procedures that confirms the presence of disease and identify the correct tumor type, location, extent and stage which will help physician to give the appropriate treatment. Biopsy, imaging tests, nuclear medicine scans, tumor biomarker tests are some of the diagnostic tests used for cancer diagnostics. According to the estimation of National cancer institute, in US around 1.6 million new cases of cancer are diagnosed, and 595,690 people have died due to cancer in 2016. Canada has estimated 202,400 new cases of cancer and nearly 78,000 deaths according to Canadian cancer society in 2016. While in Europe, 1.3 million people were diagnosed in 2015. According to National cancer institute, nearly 60% new cases of cancer are from Asia, Africa, Central and South American countries and nearly 70% of cancer deaths are also from this region. China has witnessed 4.3 million new cases of cancer and 2.8 million deaths in 2015. According to Indian council for medical research, India accounts for 1.4 million new cases of cancer and 736,000 cancer related death in 2016.

The cancer diagnostics market is booming due to increasing incidence of cancer globally, growing elderly population across the globe, increased use of personalized medicine in clinical practice, and development of new novel technologies such as nanotechnology. However, lack of skilled labors and high cost of diagnosis are some of the factors hampering the market growth to an extent.

Market Analysis: The “Global Cancer Diagnostics Market” is estimated to witness a CAGR of 11.6% during the forecast period 2018–2024. The market is analyzed based on four segments – method of diagnosis, application, end-user and regions.

Regional Analysis: The regions covered in the report are North America, Europe, Asia Pacific, and Rest of the World (RoW). The North America is set to be the leading region for the cancer diagnostics market growth followed by Europe, Asia Pacific and Rest of the World.

Method of diagnosis Analysis: The global Cancer Diagnostics market by method of diagnosis is segmented into tumor biomarker tests, tissue diagnostics (biopsy), liquid biopsy, imaging, and others. Imaging occupied the largest share in 2017, and liquid biopsy is expected to grow at a high CAGR in the coming years due to high preference of molecular based non-invasive tests, and increasing adoption of personalized medicine. Imaging is further segmented into magnetic resonance imaging, computed tomography, ultrasound, mammography, and nuclear imaging.

Application Analysis: The global cancer diagnostics market by application is segmented into lung cancer, breast cancer, Colorectal cancer, prostate cancer and others. Lung cancer occupied the largest share in 2017, and breast cancer application is expected to be fastest growing segment during the forecasted period.

End-Users Analysis: The global cancer diagnostics market by end-users is segmented into Hospitals, diagnostic laboratories, academic & research institutes and others. Hospitals occupies a major share of cancer diagnostics market in 2017 and is expected to be same for next five years.

Key Players: F. Hoffmann-La Roche Ltd, Abbott Laboratories, Inc., Siemens Healthineers (Siemens AG), Thermo Fisher Scientific, Inc., GE Healthcare, Qiagen N.V., Agilent Technologies, Inc., Hologic, Inc., Koninklijke Philips N. V. and other predominate & niche players.

Competitive Analysis: Currently, the imaging dominates the global cancer diagnostics market. The existing leading players and other predominant market players are concentrating on this market to offer advanced products. The key market players are acquiring other companies to enhance their product portfolio and strengthen their leadership position in the market. Apart from this, key players are also launching new products to have edge in this market. For instance, in July 2017, the MEDITE Cancer Diagnostics, Inc., announced the launch of SureCyte C1 fluorogenic instant staining product universally. In April 2017, Roche announced the launch of anti-p504s (SP116) Rabbit Monoclonal Primary Antibody, for the diagnosis of prostate cancer.

Benefits: The report provides complete details about the usage and adoption rate of cancer diagnostics products in various applications and regions. With that, key stakeholders can know about the major trends, drivers, investments, vertical player’s initiatives, government initiatives toward the product adoption in the upcoming years along with the details of commercial products available in the market. Moreover, the report provides details about the major challenges that are going to impact on the market growth. Additionally, the report gives the complete details about the key business opportunities to key stakeholders to expand their business and capture the revenue in the specific verticals to analyze before investing or expanding the business in this market.

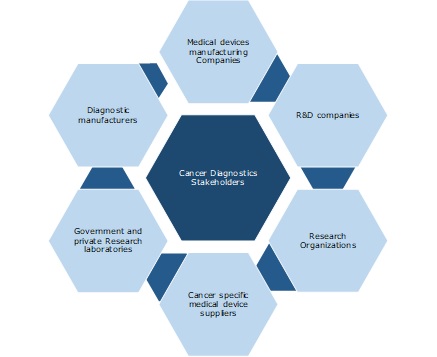

Key Stakeholders:

1 INDUSTRY OUTLOOK

1.1 Industry overview

1.2 Total addressable market

1.3 Industry Trends

2 Report Outline

2.1 Report Scope

2.2 Report Summary

2.3 Research Methodology

2.4 Report Assumptions

3 Market Snapshot

3.1 Market Definition – Infoholic Research

3.2 Advantage of cancer diagnostics

3.3 Disadvantage of cancer diagnostics

3.4 Segmented Addressable Market (SAM)

3.5 Trends of the cancer diagnostics market

3.6 Related Markets

3.6.1 Companion diagnostics

3.6.2 Genetic testing

3.6.3 Point-of-Care Diagnostics

4 Market Outlook

4.1 Overview

4.2 Funding scenario

4.3 Market segmentation

4.4 PEST Analysis

4.5 Porter 5(Five) Forces

5 Market Characteristics

5.1 DRO – Global Cancer Diagnostics Market Dynamics

5.1.1 Drivers

5.1.1.1 Rising incidence of cancer globally

5.1.1.2Growing geriatric population

5.1.1.3 Growing demand of personalized medicine

5.1.2 Opportunities

5.1.2.1 Revolutionary nanotechnology in cancer diagnostics

5.1.2.2 Increasing medical tourism

5.1.3 Restraints

5.1.3.1 High cost of diagnosis

5.1.3.2 Lack of skilled professionals

6 Method of Diagnosis: Market Size and Analysis

6.1 Overview

6.2 Tumor biomarker tests

6.3 Tissue diagnostics

6.4 Liquid biopsy

6.5 Imaging

6.5.1 Magnetic resonance imaging (MRI)

6.5.2 Computed tomography (CT)

6.5.3 Ultrasound

6.5.4 Mammography

6.5.5 Nuclear imaging

6.6 Others

7 Application: Market Size and Analysis

7.1 Overview

7.2 Lung cancer

7.3 Breast cancer

7.4 Colorectal cancer

7.5 Prostate cancer

7.6 Others

8 End Users: Market Size and Analysis

8.1 Overview

8.2 Hospitals

8.3 Diagnostic Laboratories

8.4 Academic & research institutes

8.5 Others

9 Regions: Market Size and Analysis

9.1 Overview

9.2 North America

9.2.1 Overview

9.2.2 US

9.2.3 Canada

9.3 Europe

9.3.1 Overview

9.3.2 UK

9.3.3 Germany

9.3.4 France

9.3.5 Spain

9.4 APAC

9.4.1 Overview

9.4.2 India

9.4.3 China

9.5 Rest of the World

10 Competitive Landscape

10.1 Overview

11 Vendor Profiles

11.1 F.Hoffmann-La Roche Ltd

11.1.1 Overview

11.1.2 Business Unit

11.1.3 Geographic Presence

11.1.4

11.1.5 Business Focus

11.1.6 SWOT Analysis

11.1.7 Business Strategy

11.2 Abbott Laboratories

11.2.1 Overview

11.2.2 Business Unit

11.2.3 Geographic Presence

11.2.4 Business Focus

11.2.5 SWOT Analysis

11.2.6 Business Strategy

11.3 Siemens Healthineers (Siemens AG)

11.3.1 Overview

11.3.2 Business Units

11.3.3 Geographic Presence

11.3.4 Business Focus

11.3.5 SWOT Analysis

11.3.6 Business Strategy

11.4 Thermo Fisher Scientific Inc.

11.4.1 Overview

11.4.2 Geographic Presence

11.4.3 Business Focus

11.4.4 SWOT Analysis

11.4.5 Business Strategies

11.5 GE Healthcare

11.5.1 Overview

11.5.1.1 Business unit

11.5.1.2Business focus

11.5.1.3 SWOT analysis

11.5.2 Business Strategy

12 Companies to Watch For

12.1 Qiagen N.V.

12.1.1 Overview

12.2 BioMerieux S.A.

12.2.1 Overview

12.2.2 BioMerieux S.A.: Recent Developments

12.3 Agilent Technologies, Inc

12.3.1 Overview

12.3.2 Agilent Technologies: Recent Developments

12.4 Becton Dickinson and Company

12.4.1 Overview

12.4.2 Becton dickenson and company: Recent Developments

12.5 Hologic Inc.

12.5.1 Overview

12.5.2 Hologic Inc.: Recent Developments

12.6 Illumina, Inc.

12.6.1 Overview

12.6.2 Illumina Inc.: Recent Developments

12.7 Koninklijke Philips N.V.

12.7.1 Overview

12.7.2 Koninklijke Philips N.V.: Recent Developments

13 Annexure

13.1 Abbreviations

Research Framework

Infoholic research works on a holistic 360° approach in order to deliver high quality, validated and reliable information in our market reports. The Market estimation and forecasting involves following steps:

- Data Collation (Primary & Secondary)

- In-house Estimation (Based on proprietary data bases and Models)

- Market Triangulation

- Forecasting

Market related information is congregated from both primary and secondary sources.

Primary sources

involved participants from all global stakeholders such as Solution providers, service providers, Industry associations, thought leaders etc. across levels such as CXOs, VPs and managers. Plus, our in-house industry experts having decades of industry experience contribute their consulting and advisory services.

Secondary sources

include public sources such as regulatory frameworks, government IT spending, government demographic indicators, industry association statistics, and company publications along with paid sources such as Factiva, OneSource, Bloomberg among others.

![]()