Transplant Diagnostics Market 2017-2023

- November, 2017

- Domain: Healthcare - Diagnostics

- Get Free 10% Customization in this Report

The transplantation diagnostics market is booming due to the growing patient base for chronic disease globally, growing elderly population, and the increasing number of organ transplantation procedures. High cost of sequencing instrument, requirement of skilled labors, and the difference between organs donated and patients waiting for transplantation are some of the factors hampering the market growth. The market in emerging countries is expected to grow at a rapid pace during the forecast period due the increasing healthcare awareness among public, growing patient pool, and the increasing healthcare spending.

Market Analysis

The “Global Transplantation Diagnostics Market” is estimated to witness a CAGR of 10.9% during the forecast period 2017–2023. The market is analyzed based on six segments, namely technology, products, screening methods, application, end-users, and regions.

Regional Analysis

The regions covered in the report are North America, Europe, Asia Pacific, and Rest of the World (RoW). North America is set to be the leading region for the transplantation diagnostics market growth followed by Europe. Asia Pacific and RoW are set to be the emerging regions.

Technology Analysis

The global transplantation diagnostics market by technology is segmented into molecular assays and non-molecular assays. Molecular assays include PCR-based and sequencing-based assays. Molecular assays occupy the largest share in 2016 due to its better sensitivity, specificity, and high resolving power.

Product Analysis

The global transplantation diagnostics market by product type is segmented into instruments, consumables & reagents, and softwares and services. Reagents and consumables occupy the major market share in 2016 due to repeat purchase of the consumables and reagents to perform the tests.

Screening Method Analysis

The global transplantation diagnostics market by screening method is segmented into pre-transplantation screening and post-transplantation screening. Post-transplantation screening occupies the major market share in 2016.

Application Analysis

The global transplantation diagnostics market by application is segmented into diagnostic and research applications. Diagnostic application occupies the largest market share and is expected to be the fastest growing segment during the forecast period.

End-users Analysis

The global transplantation diagnostics market by end-users is segmented into hospital & transplant centers, commercial service providers, and academics and research laboratories. Hospital and transplant centers occupy a major share of transplantation diagnostics market in 2016 due to an increase in surgical procedures.

Key Players

Thermo Fisher Scientific, Inc., Illumina, Inc., Bio-Rad Laboratories, Inc., Immucor, Inc., CareDx, Inc., Abbott Laboratories, Qiagen N.V., bioMerieux S.A., F. Hoffmann-La Roche, Omixon Ltd, and other predominate & niche players.

Competitive Analysis

Currently, the diagnostic assays based on molecular method dominates the global transplantation diagnostics market. A lot of new players are concentrating on this market to provide innovative tests to detect acute rejection within few weeks of transplantation with high sensitivity and specificity. The key market players are acquiring small companies to enhance their product portfolio and strengthen their leadership position in the market. Apart from this, major players are launching innovative tests to have an edge in the market. For instance, in February 2017, Immucor Inc. launched MIA FORA NGS FLEX HLA Typing Assay that provides comprehensive coverage of up to 11 HLA genes. The company also launched molecular gene expression assay, kidney Solid Organ Response Test (kSORT), to predict organ rejection and graft injury in May 2016.

Benefits

The report provides complete details about the usage and adoption rate of transplantation diagnostics products in various applications and regions. With that, the key stakeholders can know about the major trends, drivers, investments, vertical player’s initiatives, and government initiatives toward test adoption in the upcoming years along with the details of commercial tests available in the market. Moreover, the report provides details about the major challenges that are going to impact on the market growth. Additionally, the report gives complete details about the key business opportunities to key stakeholders to expand their business and capture the revenue in the specific verticals to analyze before investing or expanding the business in this market.

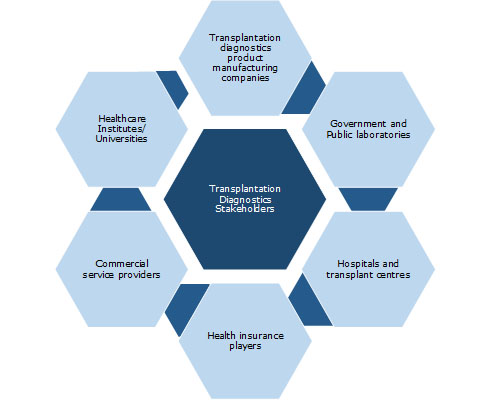

Key Stakeholders

1.1 Industry Overview

1.2 Total Addressable Market

1.3 Industry Trends

2 Report Outline

2.1 Report Scope

2.2 Report Summary

2.3 Research Methodology

2.4 Report Assumptions

3 Market Snapshot

3.1 Market Definition – Infoholic Research

3.2 Importance of Transplantation Diagnostics

3.3 Limitations of Transplantation Diagnostics

3.4 Segmented Addressable Market

3.5 Trends in the Transplantation Diagnostics Market

3.6 Related Markets

3.6.1 Liquid Biopsy

3.6.2 Cell-free DNA Testing

3.6.3 Point-of-Care Diagnostics

4 Market Outlook

4.1 Overview

4.2 Recent Product Launches

4.3 Market Segmentation

4.4 PEST Analysis

4.5 Porter 5 (Five) Forces

5 Market Characteristics

5.1 DRO Analysis

5.1.1 Drivers

5.1.1.1 Growing patient base suffering from chronic diseases

5.1.1.2 Increasing number of organ transplantation procedures

5.1.1.3 Growing elderly population

5.1.2 Opportunities

5.1.2.1 New test development and launch

5.1.2.2 Increasing adoption of modern techniques for HLA typing

5.1.3 Restraints

5.1.3.1 High cost of sequencing instrument and requirement of skilled labors

5.1.3.2 Difference between organs donated and patients waiting for transplantation

6 Technology: Market Size and Analysis

6.1 Overview

6.2 Molecular Assays

6.2.1 PCR-based Molecular Assays

6.2.2 Sequencing-based Molecular Assays

6.3 Non-molecular Assays

7 Products: Market Size and Analysis

7.1 Overview

7.2 Instruments

7.3 Consumables & Reagents

7.4 Software & Services

8 Screening Methods: Market Size and Analysis

8.1 Overview

8.2 Pre-transplantation Screening

8.3 Post-transplantation Screening

9 Application: Market Size and Analysis

9.1 Overview

9.2 Diagnostic Applications

9.3 Research Applications

10 End-users: Market Size and Analysis

10.1 Overview

10.2 Hospital & Transplantation Centers

10.3 Academic Institutions & Research Laboratories

10.4 Commercial Service Providers

11 Regions: Market Size and Analysis

11.1 Overview

11.2 North America

11.2.1 Overview

11.2.2 US

11.2.3 Canada

11.3 Europe

11.3.1 Overview

11.3.2 UK

11.3.3 Germany

11.3.4 France

11.3.5 Spain

11.4 Asia Pacific

11.4.1 Overview

11.4.2 India

11.4.3 China

11.5 Rest of the World

11.5.1 Overview

11.5.2 Brazil

11.5.3 Middle East

12 Competitive Landscape

12.1 Overview

13 Vendor Profiles

13.1 Thermo Fisher Scientific Inc.

13.1.1 Overview

13.1.2 Geographic Revenue

13.1.3 Business Focus

13.1.4 SWOT Analysis

13.1.5 Business Strategies

13.2 Illumina Inc.

13.2.1 Overview

13.2.2 Geographic Revenue

13.2.3 Business Focus

13.2.4 SWOT Analysis

13.2.5 Business Strategies

13.3 Bio-Rad Laboratories

13.3.1 Overview

13.3.2 Business Units

13.3.3 Geographic Revenue

13.3.4 Business Focus

13.3.5 SWOT Analysis

13.3.6 Business Strategies

13.4 Immucor Inc.

13.4.1 Overview

13.4.2 Business Units

13.4.3 Geographic Revenue

13.4.4 Business Focus

13.4.5 SWOT Analysis

13.4.6 Business Strategies

13.5 CareDx, Inc.

13.5.1 Overview

13.5.2 Business Units

13.5.3 Geographic Revenue

13.5.4 Business Focus

13.5.5 SWOT Analysis

13.5.6 Business Strategies

14 Companies to Watch for

14.1 Abbott Laboratories (Abbott)

14.1.1 Overview

14.2 Qiagen N.V.

14.2.1 Overview

14.3 bioMerieux S.A.

14.3.1 Overview

14.4 F. Hoffmann-La Roche

14.4.1 Overview

14.5 Omixon Ltd.

14.5.1 Overview

Annexure

Abbreviations

Research Framework

Infoholic research works on a holistic 360° approach in order to deliver high quality, validated and reliable information in our market reports. The Market estimation and forecasting involves following steps:

- Data Collation (Primary & Secondary)

- In-house Estimation (Based on proprietary data bases and Models)

- Market Triangulation

- Forecasting

Market related information is congregated from both primary and secondary sources.

Primary sources

involved participants from all global stakeholders such as Solution providers, service providers, Industry associations, thought leaders etc. across levels such as CXOs, VPs and managers. Plus, our in-house industry experts having decades of industry experience contribute their consulting and advisory services.

Secondary sources

include public sources such as regulatory frameworks, government IT spending, government demographic indicators, industry association statistics, and company publications along with paid sources such as Factiva, OneSource, Bloomberg among others.

![]()