Global Arthroscopy Devices Market Forecast up to 2025

- February, 2019

- Domain: Healthcare - Diagnostics

- Get Free 10% Customization in this Report

[110 pages report] This market research report identifies Johnson & Johnson (DePuy Synthes Inc.), Stryker, Zimmer Biomet Holdings Inc., Smith and Nephew, Inc., and Arthrex, Inc., as the major vendors operating in the global arthroscopy devices market. This report also provides a detailed analysis of the market by product types (arthroscopes, arthroscopy implants, arthroscopy visualization systems, arthroscopic shavers, arthroscopic radiofrequency systems, and arthroscopy fluid management systems), by applications (knee, hip, spine, shoulder, ankle, and sports medicine), by end-users (hospitals, ambulatory care, and trauma centers), and by regions (North America, Europe, APAC, and Rest of the World).

Research Overview

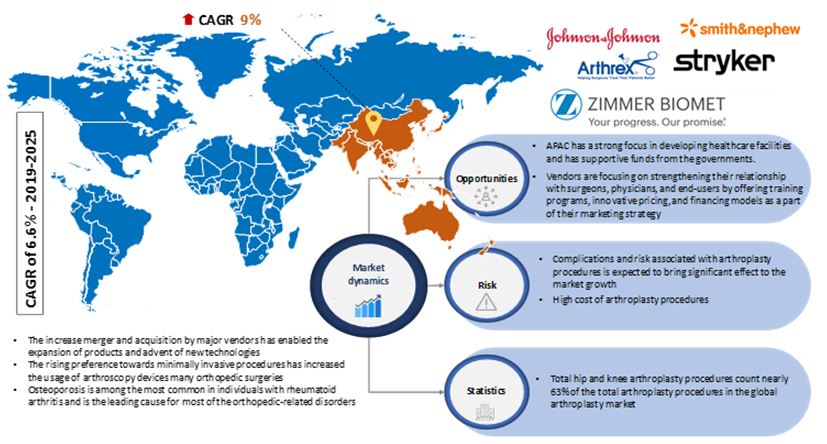

Infoholic Research predicts that the Global Arthroscopy Devices Market will grow at a CAGR of 6.6% during the forecast period. The growing popularity of minimally invasive surgical procedures has increased the usage of Arthroscopy Devices globally. These devices have helped surgeons in treating various orthopedic conditions such as osteoarthritis, bone cancer herniated discs, and other joint-related orthopedic-targeted diseases. Arthroscopy Devices have increased the interest of minimally invasive procedures; few of the popular methods among them include Shoulder Arthroscopy, Spine Arthroscopy, Knee Arthroscopy, and Hip Arthroscopy. According to the report by National Survey of Ambulatory Surgery, more than 1 million knee arthroscopic procedures are performed annually. A majority of the surgical procedures are performed based on physical examination followed by Magnetic Resonance Imaging (MRI) that gives a confirmatory diagnosis. Performing office-based needle arthroscopy has proven to be the alternative approach to visualize intra-articular pathology and anatomy in real-time. Surgical Knee Arthroscopy is the most common procedure performed.

Most of the large joint replacement implants are surgically performed when the joint is worn out or becomes dysfunctional due to injuries. Surgeries are primarily carried out to restore mobility and relieve pain. In minimally invasive surgery, a smaller surgical incision is made, and fewer muscles around the joint are detached or cut. Despite this difference, both traditional and minimally invasive joint replacement are technically demanding due to the outcomes and are dependent on the operating team with considerable experience.

According to Infoholic Research analysis, North America accounted for the largest share of the Global Arthroscopy Devices Market in 2018. The primary reasons behind the Market’s growth in the Americas are rise in the aging population, increasing incidences of osteoporosis, Advanced Healthcare Infrastructure, and rising demand for minimally invasive surgeries. The Asia Pacific region is expected to witness the fastest growth rate due to large patient pool, increasing awareness, and rising healthcare expenditure.

Segmentation by Product Types

- Arthroscopes

- Arthroscopy Implants

- Arthroscopy Visualization Systems

- Arthroscopic Shavers

- Arthroscopic Radiofrequency Systems

- Arthroscopy Fluid Management Systems

In 2018, the Arthroscopy implants segment occupied the largest share due to increase in the incidence of musculoskeletal disorders, demand for artificial knee/hip implants, and awareness about the supreme quality range of implants available in the market. Further, the radiofrequency and fluid management arthroscopy systems are expected to gain the highest volume sales during the forecast period.

Segmentation by Applications

- Knee

- Hip

- Spine

- Shoulder

- Ankle

- Sports Medicine

In 2018, the knee segment accounted for the maximum share with increased use of Arthroscopy procedures for total knee replacement.

Segmentation by End-users

- Hospitals

- Ambulatory Care

- Trauma Centers

In 2018, hospitals gained the highest share in the Arthroscopy Devices Market with the largest diagnostic volumes globally.

Segmentation by Regions

- North America

- Europe

- APAC

- RoW

The Arthroscopy Devices Market in Rest of the World is growing at a moderate pace. Despite the relevant consequences of the increasing utilization of orthopedic devices, the awareness and prevention of various ortho-related diseases are less known in South America. Middle East and Africa has significant opportunities for various orthopedic procedures. Extremities, knee, hip, foot and ankle, and sports injuries have become common and have revolutionized the early treatment of various chronic disorders.

Competitive Analysis

The Global Arthroscopy Devices Market has a broad range of surgical procedures that lead to stiff competition among vendors. The increasing awareness and availability of arthroscopic procedures are driving the competition in the market. It has a potential opportunity to grow in both developed and developing regions. The sales of arthroscopy devices are expected to increase through physician-owned orthopedic implant distributorships. Further, this model will help companies to enter partnerships with physicians, who obtain orthopedic implants from manufacturers at a low price compared to their market price. This helps companies in saving costs by eliminating the concept of the direct sales force. The growing importance of minimally invasive procedures has led to increased adoption of arthroscopy devices, resulting in the development of safe and easy to operate process and quick treatment in less time.

The competitive advantage is primarily due to the increase in mergers & acquisitions that have increased the product launch and product portfolio expansion in leading companies. For instance, in November 2018, Stryker announced the acquisition of K2M; and similarly in October 2018, it completed the acquisition of Invuity Inc. Further, customized implants are gaining benefits in premium pricing with less annual pressure.

Key Vendors

- Johnson & Johnson (DePuy Synthes Inc.)

- Stryker

- Zimmer Biomet Holdings Inc.

- Smith & Nephew Inc.

- Arthrex Inc.

Key Competitive Facts

- The market is highly competitive with all the players competing to gain the market share. Intense competition, rapid advancements in technology, frequent changes in government policies, and the prices are key factors that confront the market.

- The requirement of high initial investment, implementation, and maintenance cost in the market are also limiting the entry of new players.

Benefits

The report provides complete details about the usage and adoption rate of arthroscopy devices. Thus, the key stakeholders can know about the major trends, drivers, investments, vertical player’s initiatives, and government initiatives toward the medical devices segment in the upcoming years along with details of the pureplay companies entering the market. Moreover, the report provides details about the major challenges that are going to impact the market growth. Additionally, the report gives complete details about the key business opportunities to key stakeholders in order to expand their business and capture the revenue in specific verticals, and to analyze before investing or expanding the business in this market.

Key Takeaways

- Understanding the potential market opportunity with precise market size and forecast data.

- Detailed market analysis focusing on the growth of the arthroscopy devices industry.

- Factors influencing the growth of the arthroscopy devices market.

- In-depth competitive analysis of dominant and pure-play vendors.

- Prediction analysis of the arthroscopy devices industry in both developed and developing regions.

- Key insights related to major segments of the arthroscopy devices market.

- The latest market trend analysis impacting the buying behavior of the consumers.

Key Stakeholders

1 Industry Outlook

1.1 Orthopedic Devices

1.1.1 Overview

1.1.2 Geography

1.1.3 Medical Technologies

1.1.4 Increase in Mergers & Acquisitions

1.1.5 Industry Trends

1.2 Healthcare Spending in the US

1.3 Regulatory Bodies & Standards

1.4 Reimbursement Scenario

1.5 Third-party Reimbursement

1.6 Emerging Global Markets

1.7 Patient Demographics

1.8 Definition: Arthroscopy

1.8.1 Arthroscopy

1.8.1.1 Overview

1.8.2 Why arthroscopy?

1.9 PESTLE Analysis

2 Report Outline

2.1 Report Scope

2.2 Report Summary

2.3 Research Methodology

2.4 Report Assumptions

3 Market Snapshot

3.1 Total Addressable Market (TAM)

3.1.1 Importance of Orthopedic Devices

3.1.2 Key Facts

3.2 Segmented Addressable Market (SAM)

3.2.1 Key Highlights

3.3 Related Markets

3.3.1 Surgical Devices Market

3.3.2 Biomaterial Market

3.3.3 Hip Replacement Market

3.3.4 Dental Implant Market

3.3.5 Energy-based Aesthetic Devices Market

3.3.6 Spine Orthopedic Devices Market

3.4 Porter 5 (Five) Forces

4 Market Characteristics

4.1 Market Segmentation, By Product Type

4.1.1 Quick Facts

4.1.2 Arthroscopes

4.1.3 Arthroscopy Implants

4.1.4 Arthroscopy Visualization System

4.1.5 Arthroscopic Shavers

4.1.6 Arthroscopy Radiofrequency System

4.1.7 Arthroscopy Fluid Management System

4.2 Arthroscopy Devices Market, By Application Type

4.2.1 Knee

4.2.2 Hip

4.2.3 Spine

4.2.4 Shoulder

4.2.5 Ankle

4.2.6 Sports Medicine

4.3 Market Dynamics

4.3.1 Drivers

4.3.1.1 Increase in the Prevalence of Osteoporosis

4.3.1.1 Increasing Popularity of Arthroplasty

4.3.1.2 Rise in Elderly Population

4.3.1.3 Rise in the Number of Outpatient Procedures

4.3.2 Restraints

4.3.2.1 Complications and Risks Associated with Arthroplasty Procedures

4.3.2.1 High Cost of Arthroplasty Procedures

4.3.2.2 Inadequate Reimbursement Policies

4.3.2.1 Dearth of Skilled Professionals

4.3.3 Opportunities

4.3.3.1 Growing Popularity of Minimally Invasive Surgeries

4.3.3.2 Increase in Healthcare Spending in Improvising Healthcare Facilities

4.3.3.3 Increase in Mergers & Acquisitions

4.3.3.4 Market Expansion Opportunities in Emerging Nations

4.3.4 DRO – Impact Analysis

4.4 Key Stakeholders

5 End-Users

5.1 Overview

5.2 Hospitals

5.2.1 Key Facts

5.3 Ambulatory Care

5.4 Trauma centers

6 Regions

6.1 Overview

6.2 North America

6.2.1 Market overview

6.2.2 Key Factors

6.3 Europe

6.3.1 Market Overview

6.3.2 Key Factors

6.4 APAC

6.4.1 Market Overview

6.4.2 Key Factors

6.5 Rest of the World

6.5.1 Market Overview

6.5.2 Key Factors

7 Competitive Landscape

7.1 Competitor Comparison Analysis

8 Vendor Profiles

8.1 Johnson & Johnson (DePuy Synthes Inc.)

8.1.1 Business Units

8.1.2 Geographic Revenue

8.1.3 Business Focus

8.1.4 SWOT Analysis

8.1.5 Business Strategies

8.2 Zimmer Biomet Holdings Inc.

8.2.1 Overview

8.2.2 Business Units

8.2.3 Geographic Revenue

8.2.4 Business Focus

8.2.5 SWOT Analysis

8.2.6 Business Strategies

8.3 Stryker Corp.

8.3.1 Overview

8.3.2 Business Units

8.3.3 Geographic Revenue

8.3.4 Business Focus

8.3.5 SWOT Analysis

8.3.6 Business Strategies

8.4 Smith & Nephew Inc.

8.4.1 Overview

8.4.2 Business Units

8.4.3 Geographic Revenue

8.4.4 Business Focus

8.4.5 SWOT Analysis

8.4.6 Business Strategies

8.5 Arthrex Inc.

8.5.1 Overview

8.5.2 Business Focus

8.5.3 SWOT Analysis

8.5.4 Business Strategies

9 Companies to Watch for

9.1 Orthofix International N.V.

9.1.1 Overview

9.1.2 Key Highlights

9.1.3 Business Strategies

9.2 B. Braun

9.2.1 Overview

9.2.2 Key Highlights

9.2.3 Business Strategies

9.3 Wright Medical Group N.V.

9.3.1 Overview

9.4 OMNIlife Science

9.4.1 Overview

10 Other Vendors

Annexure

Ø Abbreviations

Research Framework

Infoholic research works on a holistic 360° approach in order to deliver high quality, validated and reliable information in our market reports. The Market estimation and forecasting involves following steps:

- Data Collation (Primary & Secondary)

- In-house Estimation (Based on proprietary data bases and Models)

- Market Triangulation

- Forecasting

Market related information is congregated from both primary and secondary sources.

Primary sources

involved participants from all global stakeholders such as Solution providers, service providers, Industry associations, thought leaders etc. across levels such as CXOs, VPs and managers. Plus, our in-house industry experts having decades of industry experience contribute their consulting and advisory services.

Secondary sources

include public sources such as regulatory frameworks, government IT spending, government demographic indicators, industry association statistics, and company publications along with paid sources such as Factiva, OneSource, Bloomberg among others.

![]()